7 reasons why ESG issues present the biggest risk for the mining sector today

Having effective digital tools and knowledgeable professionals in place is critical for mining companies’ ability to improve their ESG performance. This article explores 7 risks that companies face if they don’t adequately invest in their digital tools and workforce to effectively manage their ESG capability.

In recent years, environmental, social and governance (ESG) issues have become increasingly prominent the world over, both broadly and in the mining and metals sector.

In fact, according to a global report, 45 per cent of mining decision-makers said they thought ESG issues represented the biggest risk to the metals and mining sector today — far greater, even, than issues related to COVID-19 (Meyers, 2021). This finding is validated by EY’s most recent annual report for the sector: mining and minerals executives interviewed between June and September 2021 also saw ESG as the number one risk, followed by decarbonisation and license to operate (EY, 2021).

Resources companies around the world are under enormous and ever-growing pressure – from stakeholders, governments, employees and consumers – to reduce their power and water consumption, or find alternatives to carbon-fueled energy with green technology, and cut their overall greenhouse gas emissions.

Though progress is being made, mining still remains one of the world’s most emissions-intensive sectors, responsible for 4-7 per cent of the world’s greenhouse gas (GHG) emissions (McKinsey, 2020).

While many mining and minerals organisations are proactively committed to improving their ESG performance, the reality is that many lack the sophisticated tools to measure their emissions and identify opportunities for improvement. At the same time, regulations and compliance requirements are becoming increasingly detailed and complex.

As a result, ESG is becoming an increasing area of risk, and failure to take ESG obligations and reporting seriously could affect many organisations’ chances of future success.

In this article we share seven reasons why ESG issues are the biggest risk to the mining and minerals sector today, and explain how a metal accounting and process optimisation solution, powered by a ‘digital twin’, can help.

1. Urgent and visible pressure on mining sector to slow climate change

Climate change is a pressing global priority. The United Nations Intergovernmental Panel on Climate Change (IPCC) recently released a report showing the world is on track to reach, or exceed, 1.5°C of warming within just two decades (IPCC, 2021). According to this report, it’s only with ambitious emissions targets that we will be able to keep the world’s global temperatures to this level. A continued high-emissions scenario means the world may even warm by 4.4°C, with catastrophic results (World Resources Institute, 2021).

Historically, the mining and minerals sector has been a key contributor when it comes to emissions, and there is still very visible and growing pressure for reductions to occur. Fifty per cent of the world’s industrial greenhouse gas emissions have been traced to just 50 companies in heavy fossil fuel industries, including 20 mining companies (S&P Global, 2020a).

This doesn’t mean the industry isn’t making great progress. In fact, over 36 per cent of the world’s largest mining companies either claim to be carbon neutral already, or have set goals to reach net-zero emissions, mostly before 2050 (S&P Global, 2020b).

However, the pressure on mining companies to report on and actively show their lower carbon emissions is a key challenge. To meet reduction targets, companies must find reliable, sophisticated ways to accurately measure and report their current emissions, as well as to test, trial and then implement solutions for improvement. Failure to do so can affect their reputation, ability to secure funding and investment, attract and retain skilled workers and even their overall productivity and control.

2. Regulations, compliance and reporting standards/frameworks are becoming increasingly complex

ESG reporting requirements are moving beyond being loose guidelines to compulsory obligations for individual jurisdictions, and in most countries, reporting on emissions is now mandatory.

We are also seeing the emergence of detailed reporting standards, frameworks and recommendations – and even taskforces – which are putting resources companies under greater pressure to report on their emissions in detail.

There can also be many different requirements – depending on an organisation’s jurisdiction and function reporting can be quite subjective, requiring that organisations build on their data and information from year to year. Many of the voluntary codes and principles also overlap, meaning it can be hard for businesses to know which apply to them.

Some of the most notable include:

The 10 sustainable development principles developed by the International Council on Mining and Metals

The ICMM has developed 10 principles that members need to meet in order to fulfil their membership requirements. Currently, members of ICMM have committed to a goal of net zero scope 1 and 2 GHG emissions by 2050 or sooner (ICMM, 2021).

Compliance framework recommended by the United Nations Task Force on Climate-Related Financial Disclosures

While climate change poses an enormous risk to the planet, it also has some far-reaching financial consequences for economies around the world.

In 2015, the United Nations Financial Stability Board set up a Task Force on Climate-Related Financial Disclosures (TCFD) (United Nations Financial Initiative, 2021). The TCFD’s aim was to ensure that companies use consistent and accurate frameworks to report and disclose their climate-related risk. Their aim is that, with standardised reporting, financial institutions will be able to control and limit their level of exposure, making the world’s economy more stable and secure (United Nations Financial Initiative, 2021).

According to Deloitte, the TCFD’s framework — once voluntary —has now become part of the regulatory framework in many countries and jurisdictions around the world, with more governments expected to enact laws and policies to embed the recommendations into legislation (Deloitte, 2021).

In its 2020 report, the TCFD reveals that nearly 60 per cent of the world’s 100 largest public companies support the TCFD, report in line with the TCFD recommendations, or both (TCFD, 2020).

The TCFD is also an important way for businesses to determine their current impact and take steps to improve.

Other voluntary reporting standards

Mining and minerals organisations can also opt to report their ESG in accordance with the standards set by the Sustainability Accounting Standards Board (SASB), as well as the Global Reporting Initiative (GRI).

The accounting standards recommended by the Greenhouse Gas Protocol

There are also several voluntary schemes which encourage organisations to disclose greater information regarding their emissions and environmental impact. This includes the Carbon Trust Standards, the CDP (previously called the Carbon Disclosure Project) and the most widely used — the Greenhouse Gas Protocol.

The Greenhouse Gas Protocol is a set of standards, guidance, tools and training, designed to help businesses and governments more effectively measure and manage their emissions.Today, the protocol is the most widely used greenhouse gas accounting standard for companies, and is used by 9 out of 10 Fortune 500 companies (Greenhouse Gas Protocol, 2021).

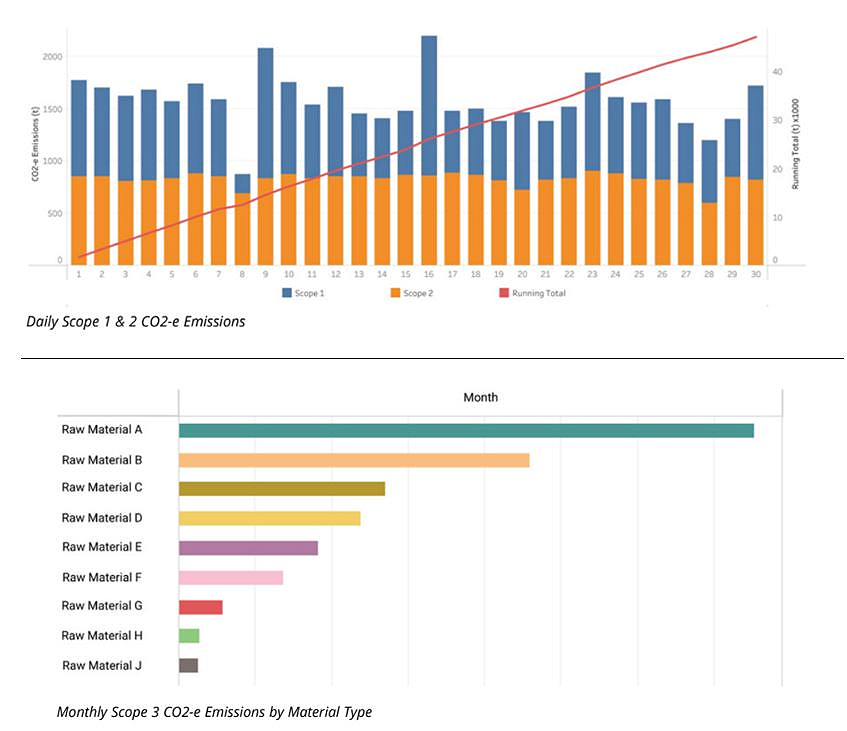

According to the protocol there are three categories or levels of emissions ‘scope’: Scope 1 (direct emissions from sources owned or controlled by the company); Scope 2 (indirect electricity emissions that physically occur at the facility where electricity is generated or from the generation of purchased electricity consumed by the company); and Scope 3 (indirect emissions that are a consequence of the activities of the company, but occur from sources not owned or controlled by the company).

Closer to home, other relevant standards/requirements include:

Mandatory reporting under the National Greenhouse and Energy Reporting Scheme

In Australia, resources companies that meet certain thresholds must also register and report their emissions and energy information under the National Greenhouse and Energy Reporting (NGER) scheme, in accordance with The Emissions and Energy Reporting System (EERS). NGER is a single national framework for reporting and sharing company information relating to greenhouse gas emissions, energy production and energy consumption (Australian Government Clean Energy Regulator, 2021).

Climate Action Plan by the Minerals Council of Australia

The Minerals Council of Australia, the leading advocate for Australia's minerals industry, has also developed a Climate Action Plan.This plan includes three overarching goals, and ten climate actions, supported by 30 individual measures over a three-year rolling work program (MCA, 2021).

AusIMM Social Responsibility Framework

AusIMM’ Social Responsibility Framework and Statement outlines that AusIMM members must be aware of and consider Environmental, Social and Governance (ESG) factors in their professional work. ESG factors include specific non-negotiable mandatory legal requirements and those contained in well-established global sustainability principles, standards and guidance.

3. Many mining companies lack sophisticated digital reporting tools

While many resources companies have a positive attitude towards digital innovation and a desire for better adoption of digital technologies, the metals and mining industry is 40 per cent less digitally mature than comparable industries (BCG, 2021).

A study by Hatch in 2020 interviewed Australian mining and minerals industry leaders and found that 72 percent of respondents said they had no digital strategy, 11 percent said they had a documented (not embraced) strategy and 17 per cent said they had an embraced strategy (Hatch, 2020). Many mining companies lack the sophisticated digital tools to be able to measure their ESG impact accurately. How can you improve your ESG credentials if you cannot measure and transparently report your activity?

Many guidelines and recommendations require organisations to build on their expertise year on year, which requires having, clean, validated and centralised plant-wide data, with end-to-end visibility with customisable and configurable reporting, analysis and data visualisation.

For many mining companies, ESG reporting is still done manually or sporadically by third party consultants. If the organisation doesn’t have a metallurgical accounting and process optimisation solution powered by a digital twin, it’s impossible to measure emissions in granular detail, accurately, transparently and consistently year on year. It’s also very difficult to identify and test ways in which the organisation can improve its ESG performance.

There are now some very powerful and sophisticated digital tools available that use the latest database structures, machine learning, AI, and cloud computing. These technologies give a strong competitive advantage, and have been implemented and proven internationally with significant returns.

4. Poor ESG credentials can affect capital and investment

As evidenced by the emergence of the TCFD, there is a strong and growing link between a company’s ability to track, measure and report its emissions and its financial prosperity. Mining companies with higher ESG ratings have an average total shareholder return 10 per cent higher than the general market index (PWC, 2021).

A recent report by McKinsey also suggests that the cost of capital can actually be up to 25 per cent higher for mining organisations with the lowest ESG scores. “Investors and lenders are increasingly focused on ESG factors when making investment decisions, which means that in many cases, in order to access capital, miners will need to demonstrate commitment to ESG concerns,” the report says (McKinsey, 2021).

There are now several third-party ratings agencies which even rank companies according to their actual or perceived ESG strengths, and a number of investment companies that have publicly committed to taking ESG ratings into account when making investment decisions.

5. Poor ESG performance linked to problems attracting and retaining staff

Currently, the mining sector creates millions of jobs around the world. However, almost half of employees are aged 45 years or older (McKenzie, 2021), and the sector runs the risk of missing out on skilled, capable workers if it fails to find a way to make mining more attractive to future generations.

The sector’s reputation across a range of ESG indicators means it isn’t particularly enticing to younger people right now. For example, to draw on the emissions discussion as an example, nearly 60% of young people say they are worried or extremely worried about climate change, and 45% say their feelings about the climate affects their daily life (Harrabin, 2021).

So in this case, being able to accurately measure – and subsequently reduce – emissions could play a key role in overcoming these negative impressions, and ensuring that young, talented people are drawn into establishing and retaining career in the mining sector.

The sector’s reputation is also very closely tied to an organisation’s overall social licence to operate – a measure of acceptance by the community that the plant is operating in. Fixing the brand of mining by showcasing strong ESG credentials will go a long way to lure more skills and talent to the profession.

6. Missed process optimisation opportunities

With powerful digital tools in place, mining organisations can extract the insights and information they need to evaluate, control and improve their ESG performance — as well as meet new regulatory frameworks and requirements.

COVID-19 has significantly accelerated digital transformation and its benefits. Accenture says that while enterprises with a strong technology focus had twice as much revenue growth as their peers before the pandemic, they are now growing five times faster than those with a slower technology uptake (Accenture, 2021).

A digital solution can support organisations with their ESG in four key areas: ensuring energy efficiency, yield improvement, reducing greenhouse gas emissions, and driving new, green processes.

Specifically, a quality solution with a digital twin at its core can help an organisation:

- Collect, validate and integrate data from every aspect of the operation, with data calculated on an hourly basis.

- Get a single, validated and well-organised source of truth for all of its GHG emissions, power and water consumption data.

- Access superior reporting and analysis tools, with dynamic, interactive and real-time calculations.

- Test scenarios to compare actual results with optimal results.

- Get visibility across the entire process and measure performance against targets.

- Get complete peace of mind that the data that is being reported to regulators is accurate and meets all the compliance guidelines.

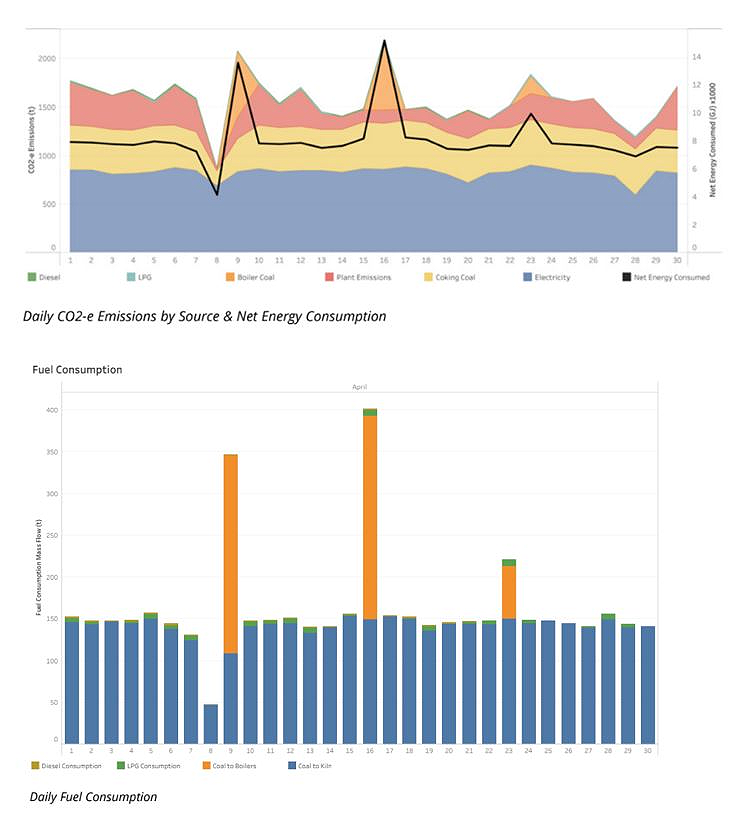

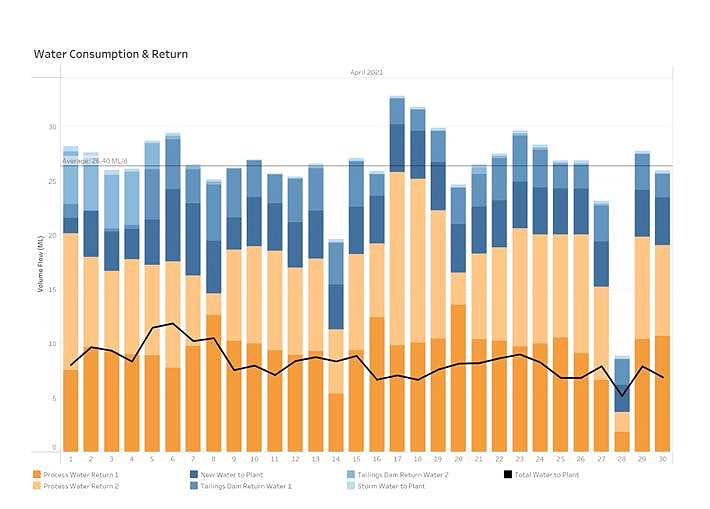

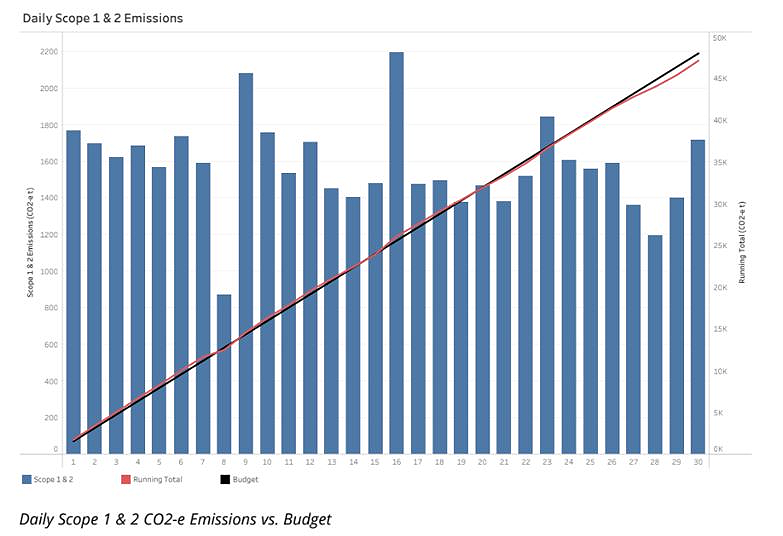

The images below, are taken from a digital dashboard, showing emissions (in accordance with the scopes specified by the Greenhouse Gas Protocol) and water consumption for a particular minerals processing plant.

It is worth noting that digital tools are only effective if they’re deployed by suitable knowledgeable persons with the skills to synthesis and understand the data. There are qualitative and quantitative factors at play in ESG performance. But with this level of detail at their fingertips, qualified professionals can accurately determine how and where to make improvements.

With an advanced digital ESG solution, it can even be possible for mining and minerals organisations to test future scenarios. This information can also be tied back to financials, so organisations can budget and forecast in accordance with ESG principles.

7. Shift in demand for critical minerals

A concerted effort to reach the goals of the Paris Agreement will mean a quadrupling of mineral requirements for clean energy technologies by 2040. And an even faster transition to net-zero globally by 2050 requires six times more mineral inputs in 2040 than today (Corrs Chambers Westgarth, 2021).

According to the International Energy Agency, clean energy technologies’ share of total demand will rise significantly over the next two decades – to over 40 per cent for copper and rare earth elements, 60 – 70 per cent for nickel and cobalt, and almost 90 per cent for lithium (Corrs, Chambers and Westgarth, 2021). A typical electric car, for instance, requires six times the mineral inputs of a conventional car, and an onshore wind plant requires nine times more mineral resources than a similarly sized gas-fired power plant (Corrs Chambers Westgarth, 2021).

When it comes to processing these finite resources, minerals companies need to be as energy efficient as possible – and the only way to do so is to have digital tools in place. Companies also need to demonstrate their care for the communities in which they are operating. Failure to adopt new, powerful systems will result in many organisations missing out on this rapidly growing market opportunity, and compromising their ESG rating.

How a metallurgical accounting and process optimisation solution, powered by a digital twin, can help

Achieving better ESG outcomes, especially when it comes to measuring emissions and consumption, is all about having the most current technology designed specifically for the minerals processing industry. With the right metallurgical accounting and process optimisation solution, with a digital twin at its heart, it’s possible to track, report and manage a plant’s emissions – as well as its power and water consumption – in very granular detail. A digital twin should also provide the ability to access all necessary information via dynamic dashboards, and to test and trial scenarios.

To thrive in the future, mining and minerals companies need to be making digital transformation – and specifically, investing in a digital twin – a critical priority. There also needs to be sufficiently skilled and knowledgeable professionals within the industry to ensure that the data captured can be effectively interpreted and acted on.

As the World Resources Institute said in a recent article, 'this is our make-or-break decade for limiting temperature rise… it’s now time for governments, businesses and investors to step up their action to be commensurate with the scale of the crisis we face.'

If you are interested in learning more about a metallurgical accounting and process optimisation – digital twin technology and how it can help your organisation take charge of its emissions, read about how Metallurgical Systems can help here.

References

Accenture, 2021. Scaling enterprise digital transformation, [online]. Available from: https://www.accenture.com/au-en/insights/technology/scaling-enterprise-digital-transformation

Australian Government Clean Energy Regulator, 2021. 'National greenhouse and energy reporting data', [online]. Available from: http://www.cleanenergyregulator.gov.au/NGER/National%20greenhouse%20and%20energy%20reporting%20data

BCG, 2021. Racing Toward a Digital Future in Metals and Mining [online]. Available from: https://www.bcg.com/en-au/publications/2021/adopting-a-digital-strategy-in-the-metals-and-mining-industry

Corrs Chambers Westgarth, 2021. IEA report highlights the increasing role of critical minerals in clean energy transition, [online]. Available from: https://corrs.com.au/insights/iea-report-highlights-the-increasing-role-of-critical-minerals-in-clean-energy-transition

Deloitte, 2021. What is the TCFD and why does it matter? [online]. Available from: https://www2.deloitte.com/ch/en/pages/risk/articles/tcfd-and-why-does-it-matter.html

EY, 2021. Top 10 business risks and opportunities, [online]. Available from: https://www.ey.com/en_gl/mining-metals/top-10-business-risks-and-opportunities-for-mining-and-metals-in-2022

Greenhouse Gas Protocol, 2021. About us, [online]. Available from: https://ghgprotocol.org/about-us

Harrabin, 2021. Climate change – young people very worried, [online]. Available from: https://www.bbc.com/news/world-58549373

Hatch, 2020. The Digital Drift: Unearthing innovative opportunities for Australia’s mining and mineral industry, [online]. Available from: https://www.hatch.com/About-Us/News-And-Media/2020/11/New-Hatch-research-reveals-opportunities-to-accelerate-digital-transformation

ICMM, 2021. Our commitment to a goal of net zero by 2050 or sooner [online]. Available from: https://www.icmm.com/

IPCC, 2021. Assessment Report AR6, [online]. Available from: https://www.ipcc.ch/assessment-report/ar6/

Minerals Council of Australia (MCA), 2021. Climate Action Plan, [online]. Available from: https://www.minerals.org.au/sites/default/files/MCA%20Climate%20Action%20Plan_Progress%20Report%202021.pdf

McKenzie, 2021. Talent trends shaping the mining industry 2021, [online]. Available from: https://www.mining.com/talent-trends-shaping-the-mining-industry-in-2021/

McKinsey, 2021. Climate risk and decarbonisation: what every mining CEO needs to know, [online]. Available from: https://www.mckinsey.com/business-functions/sustainability/our-insights/climate-risk-and-decarbonization-what-every-mining-ceo-needs-to-know

McKinsey, 2021. Creating the net zero carbon mine, [online]. Available from: https://www.mckinsey.com/industries/metals-and-mining/our-insights/creating-the-zero-carbon-mine

Meyers, 2021. Is the metals and mining industry evolving on ESG? [online]. Available from: https://www.theimpactivate.com/is-the-metals-and-mining-industry-evolving-on-esg/

PWC, 2021. Mine 2021: Great expectations, seizing tomorrow, [online]. Available from: https://www.pwc.com.au/mining/global-mine-2021.html

S&P Global, 2020a. Path to Net Zero, Miners are Starting to Decarbonise as Investor Pressure Mounts [online]. Available from: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/path-to-net-zero-miners-are-starting-to-decarbonize-as-investor-pressure-mounts-59583837

S&P Global, 2020b, Path to Net Zero, [online]. Available from: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/path-to-net-zero-more-mining-companies-setting-targets-to-reduce-emissions-61626513

TCFD, 2020. Status Report, [online]. Available from: https://assets.bbhub.io/company/sites/60/2020/09/2020-TCFD_Status-Report.pdf

United Nations Financial Initiative, 2021, [online]. Available from: https://www.unepfi.org/climate-change/tcfd/

World Resources Institute, IPCC Climate Report, [online]. Available from: https://www.wri.org/insights/ipcc-climate-report