Project and Operational ESG

ESG, shorthand for Environment, Social and Governance, is pervasive in business and financial commentary.

Unfortunately, confusion about application threatens ESG’s utility for business improvement. For instance, within the world of Exchange Traded Funds (ETFs) and related financial activity, ESG is used to describe securities portfolio management that is weighted to sectors and businesses with deemed virtuous purposes, values and products. Minerals businesses are rarely included in ESG portfolios, although applying a critical minerals banner attempts to bring some into the fold. Another finance sector application is company ESG scoring by ratings agencies based on comparisons of declared performance against broad spectrum indicators, many of which have no relevance in context.

The ESG value opportunity for minerals businesses has little to do with ‘Portfolio ESG’. Minerals sector ESG value lies in something quite different, something that can be termed ‘Project and Operational ESG’ (henceforth Operational ESG). Even here the concept is often compromised through lack of analytical rigour and poor understanding. Frequently ESG is used as a way of referring to single headline issues such as ‘climate change’, ‘human rights’ or ‘consumer protection’, often associated with some form of hard or soft sell. Such attempts at attention grabbing around single issues of pre-determined importance can lead to businesses seriously misjudging the risks that are most important to them in context.

Instead, an Operational ESG risk approach is advisable, for which a detailed description of implementation is well beyond the scope of this article. Instead, what follows is a highly simplified account of what Operational ESG is and how it can mesh with widely used management approaches.

Where does 'ESG' come from?

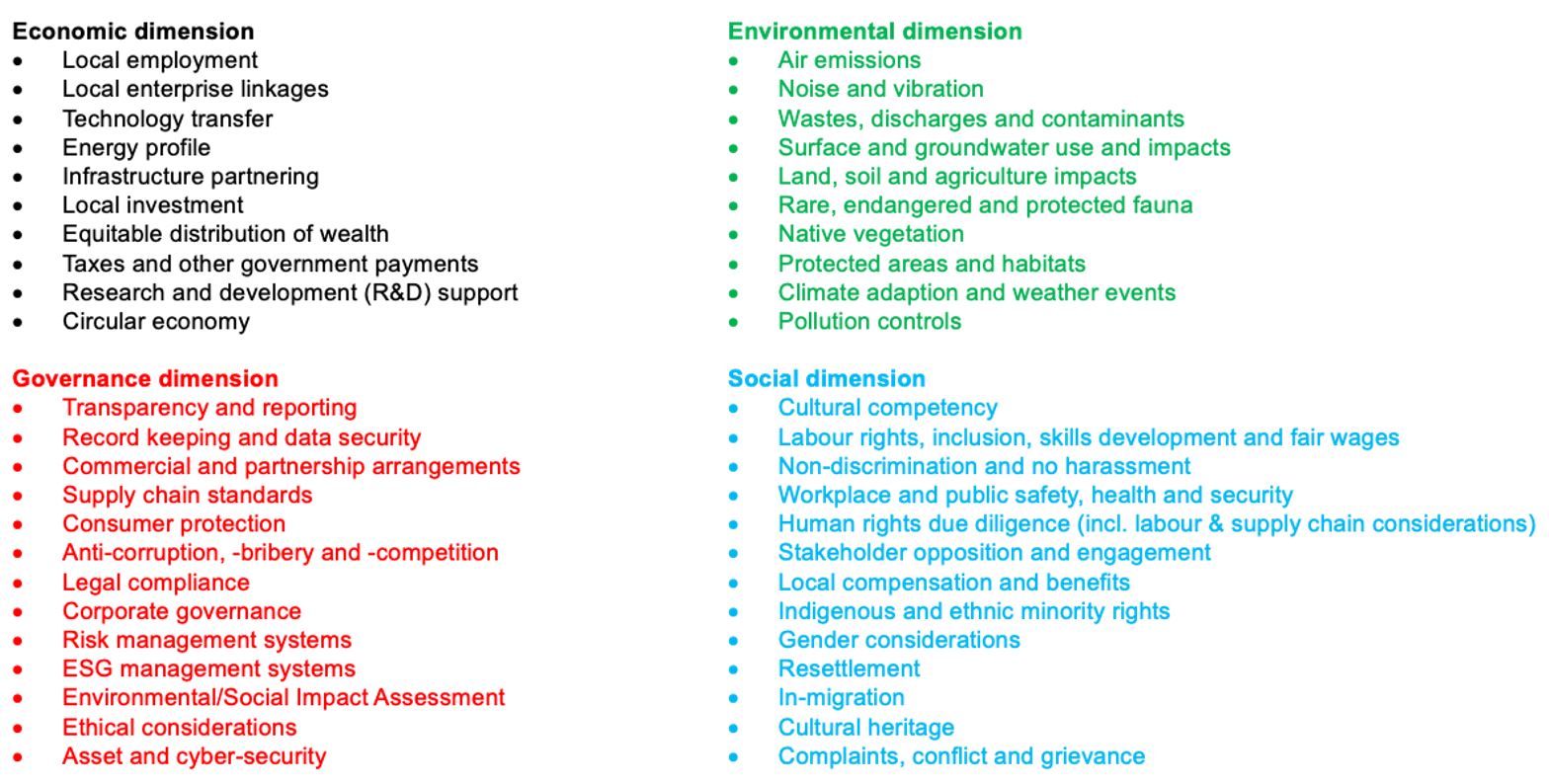

The term ESG was first used in a UN publication called ‘Who Cares Wins’ in 2004. Over the past decade it has become prominent in the business zeitgeist, indicating corporate and financial sector acceptance and adaption of the notion of sustainability, first referred to as Sustainable Development in the United Nations (UN) 1987 publication ‘Our Common Future’ (Brundtland, 1987). The publication laid the groundwork for the 1992 Rio de Janeiro Earth Summit. In the next two decades of extensive and often intense global sustainability dialogue, business was somewhat tepid in its participation, perhaps because the concept lacked the rigour of recognisable business management. This has changed in the past decade as the finance and corporate world has tacitly signalled the price for acceptance is the adoption of a more business-driven approach. This involves increasingly standardised performance metrics in each of the E, S and G dimensions alongside an economic dimension. There are currently some 46 commonly recognised (E)ESG elements with associated metrics that are relevant to the minerals sector (Fig 1).

Why is ESG important for minerals businesses?

Operational ESG when done well secures benefits for business, including reputation gain, easing regulatory approval, attracting and retaining talent who can choose where to work, securing access to debt and equity finance, and ‘social licence’ more broadly. What is not commonly appreciated is the intrinsic business benefit gained though the overall reduction in outcome variation that Operational ESG brings. The greatest source of variation for any business lies in its external environment, the things that are beyond its control. Well managed Operational ESG is a way of achieving more control and hence less variance in business interactions with the outside world.

Operational ESG

The elements listed in Figure 1 are not plucked from the air; they are adapted from a list of the most frequently referenced ESG issues identified in a meta-study of 150 investment due diligence instruments (Sauvant and Mann, 2019). Essentially, they are things referred to in orthodox economics as ‘externalities’ – things for which costs can be disproportionately borne by parties other than the primary party. For minerals businesses they are also sources of uncertainty and variance. With reference to the source-pathway-receptor model (described in J. Jeffrey Peirce et.al. 1990), gaining a high degree of control at source and pathway is the key to avoiding costly, even terminal, consequences at the receptor end of things.

Governance architecture

For a complex business to endure it must have systemic control; that is, it must be able to ensure all its workforce, including contractors, understand precisely what is expected of them in the way they carry out their work and interact with other people. This requires a cascaded set of instruction and guidance. This usually involves high-level statements of purpose and values, tightly articulated standards and assurance systems, and a voluminous body of instructive material with names like guidance notes, specifications, standard operating procedures and the like. Deeper discussion is beyond the scope of this article; suffice to say nothing that follows can occur without good governance architecture in place.

Achieving focus

Good management requires focus and 46 ESG elements cannot all be focused on at once. Hence, the first step in Operational ESG is to reduce the list of ESG issues down to what matters most in context. Context is critical – too often project proponents and operators are asking the wrong questions and responding to the wrong stimuli. Local conditions and issues are frequently overshadowed by salient (most mentioned) issues in global social media, leading to operational distraction and neglect of the most material issues in specific local context. The logical vector of analysis leading to focused attention on ESG issues that matter most in an operational context is:

- outbound impact assessment

- inbound reciprocating risk assessment

- materiality assessment

- gap analysis.

In practice, these analyses are iterative and there can be flexibility in whether impact or risk assessment comes first.

Outbound impact assessment

Direct and indirect impacts, defined as the uncertainty and effects experienced by people and the biophysical environment due to proposed activities, should be rigorously assessed as a first step in managing ESG-related issues. This might involve regulatory Environmental and Social Impact Assessment (ESIA), typically a condition of permitting, noting that regulated scope and consequent word volume can impede penetrating insight. Driven by enlightened self-interest and insight, robust ESG impact assessment starts with a good environmental and social knowledge base(line) before progressing to analysis. The 46 elements listed in Fig 1 can serve as high level prompts for the impact assessment, however tailored granularity on critical matters is recommended. Stakeholder analysis and engagement is a vital component. The involvement of competent and experienced environmental and social science professionals is essential in this and the assessments that follow.

Inbound risk assessment

Rebounding ESG-related risk, defined as the uncertainty for a business arising from its interactions with the social and biophysical environment, can be undertaken only after a business understands how it is impacting others and how they may respond. This should include regulatory, compliance, legal and contractual response. Standard risk assessment methods should be applied with proper facilitation and multi-disciplinary participation. The exercise should be directed to identifying opportunity as much as threat and inform the design of mitigating actions that will reduce any uncertainty of outcome. A good operator wants to know as precisely as possible what the outcome from undertaking a fully costed action or set of actions will be, acknowledging that prediction carries degrees of uncertainty.

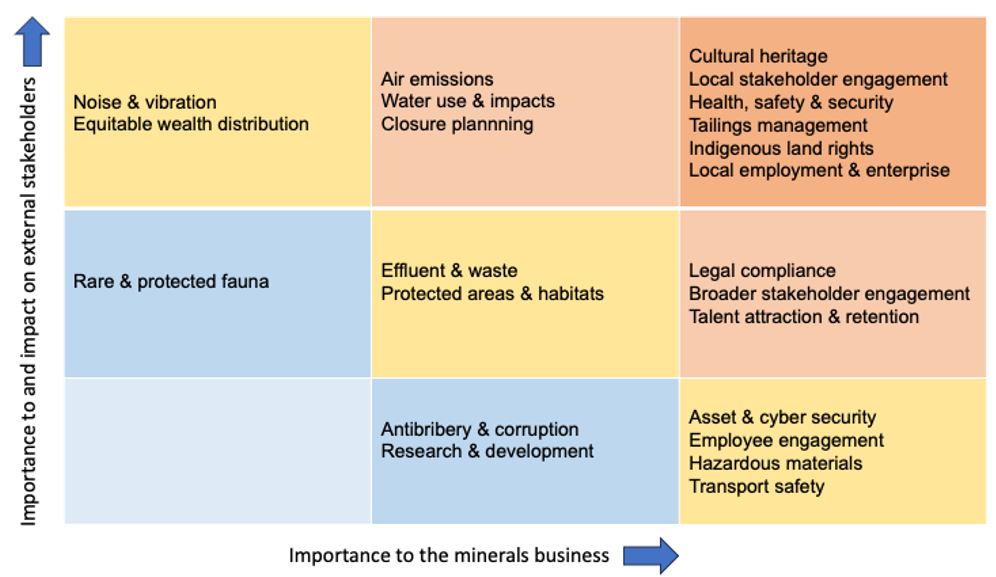

Materiality assessment

Once outbound impacts and inbound risks are identified, materiality assessment can be undertaken aiming to distinguish the most important ESG issues on which to focus. Typically, materiality assessment involves graphical representation such as the schematic example in Fig 2. The relative importance of issues for stakeholders are informed by outbound impact assessment and stakeholder engagement. The importance of issues from a business perspective are informed by the inbound ESG risk assessment and the strategic direction set out in the higher-level elements (purposes, values, standards) of a business’s governance model.

Note that material issues so identified can be ESG-related modifying factors in the context of project financing, insurance, valuation and JORC Code disclosure. For such purposes, a high degree of assessment competence and descriptive detail is recommended.

Figure 2. Example of a Materiality Assessment Diagram.

Gap analysis

Following a ranked understanding of which ESG-related issues are most material in context and require priority attention, a comparison of the desired state of control versus current state can be undertaken using orthodox gap analysis. This should progress to a list of responsive actions, broken down to ‘what’, ‘where’, ‘who’, ‘how’ and ‘when’ to form the basis of an operational ESG plan.

Operational ESG Plan

The preparation of an Operational ESG plan is the culmination of planning, inclusive of the activities described above. Planning using validated data, expertise, options analysis, and multi-disciplinary debate in the described assessment pathway is where all the value is generated. The plan merely records the results and allows for allocation of source and pathway control accountabilities into functional department plans and an overall operations plan. Integrated planning and plans are key to Operational ESG. The identification of performance tracking metrics against ESG-related actions, resourcing and accountabilities is integral to success. Taking a lead from health, safety and wellbeing disciplines, metrics for each of the ESG performance areas are rapidly becoming standardised, as published in ESG data books made available by leading companies in their integrated reporting, validated by assurance activity.

ESG Assurance

A ‘Three Lines’ assurance approach is common in the minerals sector and ESG-related matters should get the same level of scrutiny and verification as the rest of a business. For most value, a combination of audit (backward looking) and review (forward looking) elements should be present in assurance activities, properly facilitated within a collegiate atmosphere involving people experienced and competent in respective E, S and G matters. Validation of measurable performance data is vital to preserve integrity in the ESG disclosure that is now expected, summed up in the phrase - Don’t trust us, measure us.

ESG Reporting

Comprehensive ESG-related disclosure is now expected by regulators, investors, lenders, insurers and ratings agencies. While frequent material disclosure for public companies is required, an annual Sustainability Report encapsulating rolled up performance over a year with comparisons to previous years is now common practice. Better practice increasingly involves a comprehensive Integrated Report that includes all financial, technical and ESG matters with standardised metrics that allow for easy comparisons to competitor performance and temporal trends. Advanced practice extends to data books with the raw data that lies behind dashboard derivative metrics being made available for download. A surprising small number of raw data indicators (as few as 120) can provide for limitless derivative formulation. Ratings agencies and analysts have their own preferred derivative and trend indicators, hence value being able to download raw data and populate their own algorithms.

Conclusion

Operational ESG is where the rubber hits the road for minerals businesses wishing to gain broad-based trust, business certainty and secure permitting, financing, insurance and an engaged workforce. For operational personnel this short article describes how they have a vital role to play and that ESG management does not require special approaches. Commonly used analytical and operational methods apply. For people in non-operational roles or engaged in sectors peripheral to mainstream exploration, mining and minerals processing, this article serves to describe what a robust business-driven approach to ESG performance should look like.

In contrast, much of the current public commentary and cherry picking of salient (trending) issues that is presented as strategic ESG serves to distract. Unfortunately, this distraction will result in more instances of management failure at source and pathway, requiring expensive remediation, compensation and business suspension to conciliate receptors. ESG is not exotic and has no utility when deployed as strategic banner waving - it requires diligent, well-resourced competent people working in operations-directed work.

References

Brundtland, G.H. (1987) Our Common Future: Report of the World Commission on Environment and Development. Geneva, UN-Dokument A/42/427.

Jeffrey Peirce, P. Aarne Vesilind, and Ruth Weiner, 1990. Environmental Pollution and Control. Elsevier Inc.

Karl P. Sauvant and Howard Mann, 2019. Making FDI More Sustainable: Towards an Indicative List of FDI Sustainability Characteristics. The Journal of World Investment & Trade; Publication Date 17 Dec 2019. https://brill.com/view/journals/jwit/20/6/article-p916_6.xml?language=en.