Risk, and planning to not plan

Summary

Risk is ubiquitously present in establishing strategy for any asset in the mining industry. This is a function of imperfect knowledge of the deposit, numerous external factors, and the long timeframes involved. Capital investments are typically large and environmental impacts significant, therefore the potential consequences of unfavourable outcomes to the operating company, its shareholders, and impacted communities can be substantial. Incorporating the quantification of risk in the process used to establish mining strategy is far from trivial, yet it is becoming increasingly critical to the success of mining projects and operations, to the relationship between the mining industry and the broader society, and therefore to society itself being fundamentally dependant on the commodities the mining industry provides.

Effective and resilient strategy should be based on risk-informed decision making, or stated in another way, developing a strategy that does not consider risk is not very strategic.

Risk is often quantified in the financial model. This paper will demonstrate that such post-hoc approaches to quantifying risk are potentially incorrect at a fundamental level and may not appropriately quantify the intended risk. Furthermore, any post-hoc adjustments will potentially undermine all prior optimisation processes and analyses. As such post-hoc approaches, including those applied in the financial model, should not be used in isolation to support risk-based decision making.

Introduction

Incorporating risk sources in the planning framework for the evaluation of mining assets is complex. Even static planning for a mining asset is non-trivial, time-consuming, and involved. The further from Newtonian the modelling of interactions the exponentially more complex this process becomes.

When considered at a cursory level, risk-modelling can be perceived as a simple exercise; the issue is that this simplification of a complex problem can deliver answers that are demonstrably incorrect, potentially misleading, and upon deeper thought are in fact not quantifying the intended risk. Accurately quantifying risk is complex and must start with a clear definition of exactly what is to be quantified, followed by the correct execution of an appropriate experimental design.

The financial model is arguably the most obvious place to model and quantify risk; unfortunately this approach is flawed for many important sources of risk. Considering commodity price risk, if the parameters are changed, then the construct of the cut-off grade optimisation (for a metalliferous deposit – similar impacts will occur in other commodities) has changed. If the financial model is rerun using the same schedule, and therefore with the same cut-off grade policy, then the risk being quantified in the financial model is the risk of keeping the same plan while the commodity price environment is changing. It is therefore not quantifying the risk to the business of commodity price changes as a function of the optionality within the deposit and the ability of the operational team to adapt and respond.

Given that the latter is likely the intention of such an analysis, adjustments to the financial model are not quantifying the intended risk, and therefore may not be providing the required insight to guide strategic decision making. Such post-hoc analyses quantify the risk of not revising mine plans to changes in key parameters; they quantify the risk of ‘planning to not plan’. This is undoubtedly a material and very costly risk, but likely not one that most mining operators would intentionally consider as a business driver or a primary component of their strategy.

To clarify, at the first level of abstraction of commodity price risk there are two approaches: hold the schedule constant and change the price parameter(s), or re-optimise the schedule with the changed price parameter(s). The results are not the same and they do not quantify the same risk. Holding the schedule constant will quantify the risk of planning to not plan, or more concisely the commodity price risk in the selected schedule. Re-optimising the schedule will quantify the risk to the operation of changes in the commodity price inclusive of the capability of the planning and operational teams to respond to the change as a function of the deposit. The quantification of both risks are valid, however they should not be confused or considered interchangeable.

This paper will demonstrate that these two risks are different using an example based on a real-world deposit. Further differentiation of commodity related price risks is outlined in Figure 5.

Industry and literature review

“The world of planning and implementation is a highly stochastic one where things happen only with a certain probability and rarely turn out as originally intended. The failure to reflect the probabilistic nature of project planning, implementation and operation is a central cause of the poor track record” [1 - Editors note: the references in this paper are numbered for readability - please see reference list at the end of the article for full citations].

Risk in the mining industry is well considered in the literature, often in generic non-specific terms, or based on a singular risk source. Rarely is it considered at a detailed level across the wide range of potential sources of risk.

The impacts of risk on project success rates are well recognised. Badri and Nadeau [2] identify this in their paper titled “A Mining Project is a Field of Risks” in which they refer to researchers who “view the mining sector among the world’s most uncertain”. The complexity of the problems for all involved in establishing and delivering strategy for the mining industry is without question. Multiple potential sources of risk correlate, interrelate and potentially compound. If these were to be lumped into the discount rate [3] there would likely be no future mining investments; something more nuanced is clearly required. Along these lines Auger and Ignacio Guzmán [4] postulate, after reviewing the investment success of 51 copper mines, that “an additional source of ‘‘irrationality’’ may well be the tools used to make investment decisions, especially when uncertainty exists”.

Many of the more specific risks have, and continue to be, thoroughly considered in the literature. For example:

- Geological risk is particularly well represented, with numerous authors discussing impacts and approaches from multiple aspects, including [see references 5-19].

- ESG based risks have received an increased focus over recent times, with multiple authors quantifying and considering the associated risks, [including references 20-26].

- The CRC TiME (https://crctime.com.au) research program is actively investigating a wide range of risks and challenges relating to mine closure and post-mine transition and the associated impacts on a wide range of stakeholders.

A higher-level analysis in terms of both time and scale is considered by the UQ-SMI Complex Orebodies program. One component of this program considers a wide range of risks, both technical and those related to environment, social and governance (ESG), in the context of the potential impacts on achieving projections of the future supply of commodities essential to society. These risks are categorised and quantified on a comparative basis to identify deposits most impacted by varying sources of complexity, and which sources of complexity are the most pervasive. The focus of this research is on a global scale, as described by Valenta and Kemp [27], who state that after examining “308 of the world's largest undeveloped copper orebodies” they have produced “a current, comprehensive, multi-factor risk profile of the world's future copper supply”. This is impressive work, albeit with a different level of focus to the quantification of risk considered in this paper. Further information on the Complex Orebodies program can be found in the program report [28].

Scenario planning

Scenario planning [references 29-32] is a well-recognised approach to consider the potential impact of a wide range of risks and strategic alternatives. Developed to support strategic decision making under threat of potential thermonuclear war, scenario planning has been used widely by a range of industries, notably oil and gas. In the book Rethinking Strategy [30] the author strongly advocates the use of scenarios as detailed by multiple others including Herman Kahn [29], Pierre Wack [33] and Ian Wilson [31] as a method by which to understand the impacts of risk (referred to as ‘uncertainty’ in the book).

Scenario planning requires the analysis of multiple potential future scenarios, not all of which are favourable, such that as the future presents itself, the management team has already considered via scenario planning what the preferred response might be. The same scenario-based approach can be used to guide decision making for those decisions that must be made in the present that can be expected to impact future business robustness, for example this could include the size of a processing plant and the relationship to mining rates and mining stage designs.

Scenario planning is not without significant challenges when it comes to the mining industry. This comes about due to the scale and complexity of the problems and the associated time required to correctly generate an appropriate range of scenarios. This was observed by Maybee and Lowen [34] who stated that “the number of options considered for mine scheduling tends to be limited by the time available rather than establishing the risk profile surrounding a project’s potential value”. A similar observation is made by de Freitas Silva [35] who states that “due to its complexity and prohibitive size, traditional mine planning usually relies on heuristic or metaheuristic methodologies which are able to provide good solutions in a reasonable amount of time. However, most of the uncertainty that surrounds the mining complex is ignored leading to non-realistic results”.

In discussing the application of scenario planning, Tighe [30] states that scenarios are generally commonplace when “the environment is uncertain, the stakes are high, or the performers are elite”. In the practice of strategic planning for mining assets all these factors are, or should be, present. When it comes to the application however, human nature may work against us on the basis that it invariably drives us to simplify the complex. At times this can be advantageous, while in other instances it fails us. Numerous philosophical and psychological assessments ascertain this, with some of the more cited including Thinking, Fast and Slow by Daniel Kahneman [36] and The Black Swan by Nassim Nicholas Taleb [37].

Given the complexity involved in developing scenarios to incorporate risk in mine planning, this is often completed in the financial model being the quickest and easiest approach. Unfortunately, this acute simplification may not be quantifying the intended risk as outlined in the introduction.

What are you quantifying...?

In seeking to quantify any risk, if in a mathematical sense the construct of the objective function that was used to optimise any prior process is changed, the same processes must be revised for it to be correct. If not, all prior optimisation work will be invalidated by the post-hoc risk-based modification made. Furthermore, the quantification is likely flawed.

Returning to commodity price risk, if the underlying optimisation processes are revisited, likely including pit optimisation (or stope optimisation) and schedule optimisation, the risk being quantified will be the commodity price risk as a function of the deposit and the expected capability of the operation to respond. If it was quantified only in the financial model, it will represent the commodity price risk for that schedule, and therefore may misrepresent the intent of the analysis. There are clearly similarities between these two risks, and without some consideration the distinction may not be made. Both risks will be directionally consistent, and potentially of a similar magnitude, so at a superficial level the ‘quick’ approach may appear to be correct. In the case that the schedule cannot be changed, this would be the correct output, however this is rarely the case particularly for open pit assets.

In some instances, the results will in fact converge and deliver an identical result. This would be expected to occur when the boundary between profitable material and waste is very sharp and able to be extracted as such, for example in a high-grade veined gold deposit or a kimberlite pipe. As the commodity price changes the product differentiation is not impacted, the quantities of ore and waste remain the same, only the financial margin is being impacted. In such instances the schedule optimisation would not be expected to change. The same cannot be said, however, for the pit optimisation (or stope optimisation). The more gradational the changes in incremental value across the deposit, the less appropriate post-hoc analyses become.

As such, abbreviations to risk modelling introduce further risks and may not quantify the risk of interest.

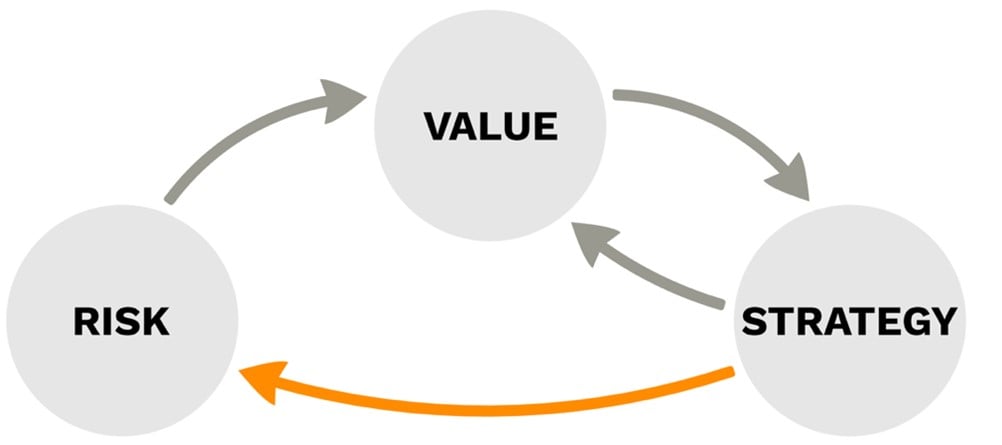

The way that risk is considered in planning processes is also an interesting point worth considering. The importance of risk to these processes is certainly recognised, arguably more so as an output of the selected plan rather than as an input to the process used to select the plan, i.e., a mine plan and strategy will often be developed, and the identified risks of the approach then quantified as an output. Correctly risk should be used to guide and inform strategy, thereby used as an input to the process as well as being quantified as a series of outputs of the selected strategy and plan. Logically risk is impacted by strategy, with both risk and strategy then impacting on value. Figure 1 [38] illustrates these relationships at a high level.

Figure 1: Schematic of the relationship between risk, value, and strategy.

Illustration of issues in post-hoc risk modelling

To illustrate the unintended impact of post-hoc modelling on risk quantification, summary level data from a real-world example is included. The numbers are based on a large open cut porphyry copper deposit and illustrate the impacts of different approaches to modifying the copper price.

The base case net present value (NPV) was optimised and modelled using the base case copper price assumption of $4,427M.

For the risk quantification all the approaches, models and inputs used were consistent except the copper price, with the risked scenario having a copper price reduced by 20% as compared to the base, with the following directly comparable NPV results:

- Post-hoc adjustment in the financial model: $934M

- Schedule optimisation adjustment only: $1,150M

- Pit and schedule optimisation adjustment: $1,239M

The post-hoc modification reduced the value by $305M more than the analysis that was re-optimised using the revised price parameter. This value reduction includes the cost of planning to not plan. If the option to change the ultimate pit is not feasible, invalidating the schedule optimisation component of the planning process through post-hoc adjustment results in an impact of $216M.

The reason for the difference is that the post-hoc adjustment fundamentally invalidates all the preceding optimisation work that was completed using the base case copper price.

Risk incorporation

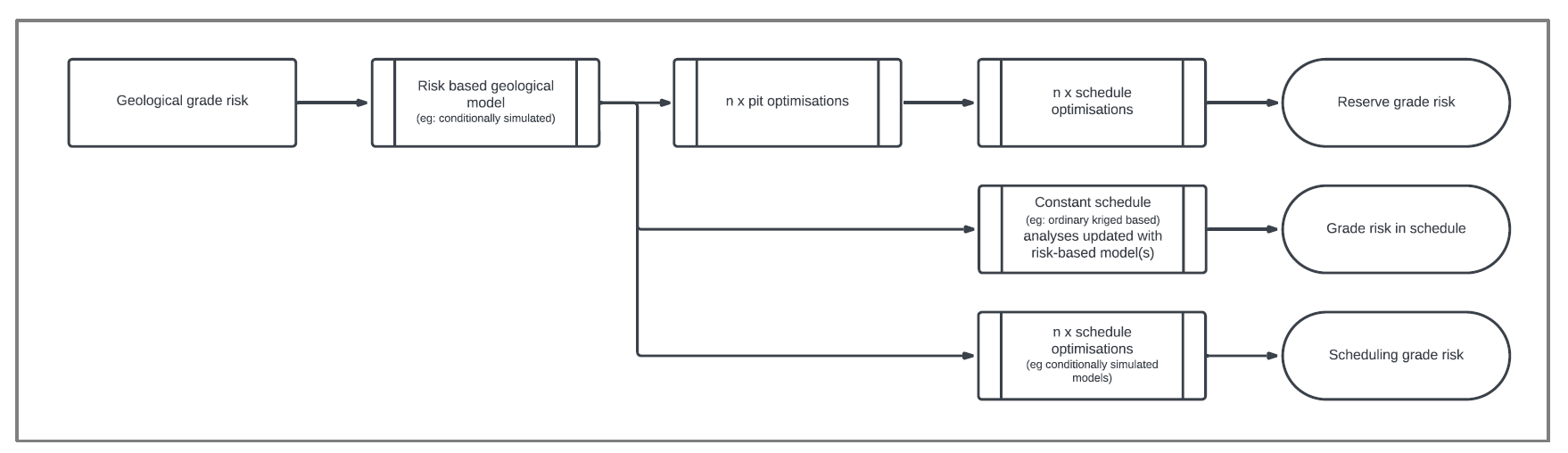

There are multiple sources of risk that can be relevant when considering strategic decisions in the mining industry. Figure 2 provides an overview of how geological grade risk might be integrated into a planning framework.

Figures 3 - 10 (available in the PDF link below) provide a non-exhaustive expansion of risk outcomes from a range of more commonly considered sources; and Table 1 summarises the same in a simplified table format.

Download all figures and tables in hi-res PDF format here

One key intention of these is to provoke further thought around the complexity and range of risks that may warrant consideration, and how these should be quantified to support strategic decision making.

Generally, risk should be incorporated at the first point of impact in the planning process. For example, if the parameter is used in the pit optimisation process, then correctly this should be re-analysed to quantify the potential impact to this component of the process and thereafter all subsequent planning components. Figure 11 illustrates the most logical mapping for a range of risk sources into a standard planning framework; note that this will not always be the correct location depending on the details of the asset and the risk being modelled.

Table 1 summarises the different range of risks outlined in Figure 2 - Figure 10 and includes in the columns ‘Pit Optimisation’, ‘Schedule Optimisation’ and ‘Financial Model’ the placement and order that different risks should be included in a planning framework. The final column then outlines the risks that can potentially be quantified.

A notable omission from the consideration of risk in planning processes as outlined in this paper is environmental risk in all forms. This is due to the variability of such risks, many of which are operation specific, and the complexity associated with the interaction with those risks that are directly associated with the mine production-based strategy being the focus of this paper. This is not to imply that such risks cannot be incorporated, or to diminish the significance of environmental risks, which is undeniable. Incorporation of environmental risks may be covered in a follow-up paper.

Discussion

A key starting point to incorporating risk in strategic planning is the quantification of these risks as a function of the strategic option being considered, and this has been explored for a range of potential risks in this paper.

Correctly quantifying risk in the process used to establish strategy for a mining asset is undeniably complex. Given the capital involved and the potential impacts to a wide range of stakeholders the associated effort is warranted.

This paper has demonstrated that simple abbreviations based on post-hoc modelling adjustments will not, in certain instances, suffice, and that a greater level of effort and diligence is required. This paper has also argued that the quantification of risk should be routinely used as an input to establish strategy as opposed to an output.

Quantifying risk in the mining investment process is complex. In that context this paper is superficial, but hopefully evokes an ongoing important thread of discussion and research in the mining industry.

Acknowledgments

The author wishes to thank Roger Higgins, Alice Clark, Daniel Hastings and Bryant Barnett for useful discussions.

Disclaimer: Bulletin articles are general in nature and not peer reviewed.

References

- Flyvbjerg, B., N. Bruzeluis, and W. Rothengatter, Megaprojects and Risk. 2011: Cambridge University Press.

- Badri, A., S. Nadeau, and A. Gbodossou, A mining project is a field of risks: a systematic and preliminary portrait of mining risks. International Journal of Safety and Security Engineering, 2012. 2(2): p. 145-166.

- Lonergan, W., Traps in mining valuations. JASSA: The Finsia Journal of Applied Finance, 2002(ISSUE 1 AUTUMN 2002).

- Auger, F. and J. Ignacio Guzmán, How rational are investment decisions in the copper industry? Resources Policy, 2010. 35(4): p. 292-300.

- David, M., Handbook of applied advanced geostatistical ore reserve estimation. 1988: Elsevier Science Publishers.

- Godoy, M., The effective management of geological risk in long-term production scheduling of open pit mines. 2002, The University of Queensland.

- Valenta, R.K., et al., Estimating Geometallurgical Risk in Undeveloped Complex Orebodies, in 14th International Mineral Processing COnference. 2018.

- Dowd, P. and P. Dare-Bryan, Planning, Designing and Optimising Production Using Geostatistical Simulation, in Advances in Applied Strategic Mine Planning, R. Dimitrakopoulos, Editor. 2018, Springer.

- Monteil, L., R. Dimitrakopoulos, and K. Kawahata, Simultaneously Optimizing Open-Pit and Underground Mining Operations Under Geological Uncertainty, in Advances in Applied Strategic Mine Planning, R. Dimitrakopoulos, Editor. 2018, Springer.

- Robins, S., Using Grade Uncertainty to Quantify Risk in the Ultimate Pit Design for the Sadiola Deep Sulfide Prefeasibility Project, Mali, West Africa, in Advances in Applied Strategic Mine Planning, R. Dimitrakopoulos, Editor. 2018, Springer.

- Spleit, M., Production Schedule Optimisation—Meeting Targets by Hedging Against Geological Risk While Addressing Environmental and Equipment Concerns, in Advances in Applied Strategic Mine Planning, R. Dimitrakopoulos, Editor. 2018, Springer.

- Tavchandjian, O., A. Proulx, and M. Anderson, Application of Conditional Simulations to Capital Decisions for Ni-Sulfide and Ni-Laterite Deposits, in Advances in Applied Strategic Mine Planning, R. Dimitrakopoulos, Editor. 2018, Springer.

- Ravenscroft, P., Risk analysis for mine scheduling by conditional simulation. International Journal of Rock Mechanics and Mining Sciences & Geomechanics Abstracts, 1992.

- Dimitrakopoulos, R., Conditional simulation algorithms for modelling orebody uncertainty in open pit optimisation. International Journal of Surface Mining Reclamation and Environment Reclamation and Environment, 1998.

- Kent, M., R. Peattie, and V. Chamberlain, Incorporating grade uncertainty in the decision to expand the main pit at the Navachab gold mine, Namibia, through the use of stochastic simulation, in Orebody modelling and strategic mine planning, R. Dimitrakopoulos, Editor. 2007, AusIMM.

- Godoy, M. and R. Dimitrakopoulos, A risk quantification framework for strategic mine planning: Method and application. Journal of mining science, 2011. 47(2): p. 235-246.

- Menabde, M., et al., Mining Schedule Optimisation for Conditionally Simulated Orebodies, in Orebody Modelling and Strategic Mine Planning - Uncertainty and Risk Management Models (2nd Edition). 2007, The Australasian Institute of Mining and Metallurgy (The AusIMM). p. 379-383.

- Godoy, M. and R. Dimitrakopoulos, A Multi-Stage Approach to Profitable Risk Management for Strategic Planning in Open Pit Mines, in Orebody Modelling and Strategic Mine Planning - Uncertainty and Risk Management Models (2nd Edition). 2007, The Australasian Institute of Mining and Metallurgy (The AusIMM). p. 337-343.

- Mai, N.L., O. Erten, and E. Topal, A new generic open pit mine planning process with risk assessment ability. International Journal of Coal Science & Technology, 2016. 3(4): p. 407-417.

- Davis, R. and D. Franks, Costs of Company-Community Conflict in the Extractive Sector. 2014.

- Krieger, N. and W. Schneller, Inside ESG Part 1: Research and Portfolio Design. 2021, FINSIA - Dimensional.

- Marsh, C. and S. Robinson, ESG and Technology: Impacts and Implications. 2021.

- Lèbre, É., et al., Source Risks As Constraints to Future Metal Supply. Environmental science & technology, 2019. 53(18): p. 10571-10579.

- Edraki, M., et al., Designing mine tailings for better environmental, social and economic outcomes: a review of alternative approaches. Journal of Cleaner Production, 2014. 84(1): p. 411-420.

- Daniel, M.F., et al., Conflict translates environmental and social risk into business costs. Proceedings of the National Academy of Sciences, 2014. 111(21): p. 7576.

- Franks, D.M., et al., Sustainable development principles for the disposal of mining and mineral processing wastes. Resources Policy, 2011. 36(2): p. 114-122.

- Valenta, R.K., et al., Re-thinking complex orebodies: Consequences for the future world supply of copper. Journal of Cleaner Production, 2019. 220: p. 816-826.

- UQ-SMI, Collaboration and impact: Complex Orebodies Program, S.M. Institute, Editor. 2022, The University of Queensland - Sustainable Minerals Institute.

- Kahn, H., Thinking about the unthinkable. 1962, New York: Horizon Press.

- Tighe, S., Rethinking Strategy. 2019: Wiley.

- Wilson, I., The subtle art of strategy : organizational planning in uncertain times. 2003, Westport, Conn.: Praeger.

- Kahneman, D., D. Lovallo, and O. Sibony, Before You Make That Big Decision. Harvard Business Review, 2011. 89(6): p. 50-60.

- Wack, P., Scenarios: Uncharted Waters Ahead. Harvard Business Review, 1985. 63(5): p. 72.

- Maybee, B., S. Lowen, and P. Dunn, Risk-based decision making within strategic mine planning. Int. J. of Mining and Mineral Engineering, 2010. 2(1).

- de Freitas Silva, M., Solving a Large SIP Model for Production Scheduling at a Gold Mine with Multiple Processing Streams and Uncertain Geology, in Advances in Applied Strategic Mine Planning, R. Dimitrakopoulos, Editor. 2018, Springer.

- Kahneman, D., Thinking, Fast and Slow. 2012: Penguin Psychology.

- Taleb, N.N., The Black Swan. Second Edition ed. 2010: Random House.

- Holloway, E.C., Risk and strategy in mineral asset optimisation and valuation, in The Sustainable Minerals Institute. 2021, The University of Queensland.